Contents

- 1 Introduction

- 2 Amalgamation

- 3 Absorption

- 4 Differences between Amalgamation and Absorption

- 5 Examples of Amalgamation and Absorption

- 6 Conclusion

- 7 Important FAQs

- 7.1 What is the difference between amalgamation and absorption?

- 7.2 How do the accounting treatments differ between amalgamation and absorption?

- 7.3 What are the legal differences between amalgamation and absorption?

- 7.4 Who gains control over assets and liabilities in amalgamation and absorption?

- 7.5 What is the impact on shareholders in amalgamation and absorption?

Looking to understand the difference between amalgamation and absorption? Our detailed blog provides insights into the accounting treatment, legal aspects, control over assets and liabilities, and impact on shareholders for both methods of corporate restructuring. Learn more now!

Introduction

In the world of business, mergers and acquisitions are common occurrences. Two common methods of combining companies are amalgamation and absorption. While they may seem similar at first glance, there are some key differences between the two. Understanding these differences can be critical in making informed business decisions.

Amalgamation

Amalgamation involves the combination of two or more companies to form a new entity. This new entity will have its own distinct legal identity and will be responsible for its own assets, liabilities, and obligations.

Types of amalgamation

There are two types of amalgamation – amalgamation in the nature of merger and amalgamation in the nature of purchase.

In amalgamation in the nature of merger, the companies involved come together to form a new entity, with the shareholders of each company becoming shareholders of the new entity. In this type of amalgamation, there is no buyer or seller, and the companies combine as equals.

In amalgamation in the nature of purchase, one company purchases the other company’s assets and liabilities. The shareholders of the company being purchased receive payment for their shares in the form of cash, shares in the purchasing company, or a combination of both.

Accounting treatment for amalgamation

The accounting treatment for amalgamation can vary depending on the type of amalgamation involved.

In amalgamation in the nature of merger, the assets and liabilities of the merging companies are transferred to the new entity at their book value. The difference between the total value of the assets and liabilities transferred and the value of the shares issued by the new entity is recorded as goodwill.

In amalgamation in the nature of purchase, the assets and liabilities of the company being purchased are recorded at their fair value, and any difference between the purchase price and the fair value of the net assets acquired is recorded as goodwill.

Absorption

Absorption is the process by which one company acquires another and incorporates it into its own operations. In this type of combination, the acquired company’s assets and liabilities become part of the acquiring company’s assets and liabilities, and the acquired company ceases to exist as a separate legal entity.

Types of absorption

There are two types of absorption – vertical absorption and horizontal absorption.

In vertical absorption, the acquiring company acquires a company that is involved in a different stage of the production process. This can allow the acquiring company to expand its operations and increase its market share.

In horizontal absorption, the acquiring company acquires a company that is involved in the same stage of the production process. This can allow the acquiring company to eliminate competition and increase its market power.

Accounting treatment for absorption

The accounting treatment for absorption involves recording the acquired company’s assets and liabilities at their fair value. Any difference between the purchase price and the fair value of the net assets acquired is recorded as goodwill.

Differences between Amalgamation and Absorption

| Difference | Amalgamation | Absorption |

|---|---|---|

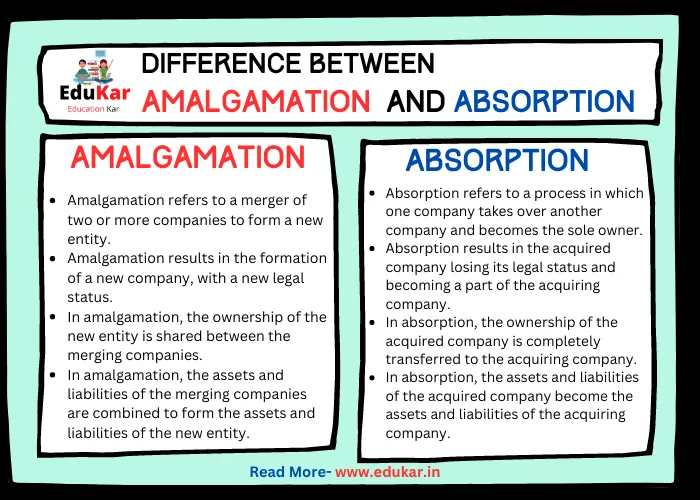

| Meaning | Amalgamation refers to a merger of two or more companies to form a new entity. | Absorption refers to a process in which one company takes over another company and becomes the sole owner. |

| Legal Status | Amalgamation results in the formation of a new company, with a new legal status. | Absorption results in the acquired company losing its legal status and becoming a part of the acquiring company. |

| Ownership | In amalgamation, the ownership of the new entity is shared between the merging companies. | In absorption, the ownership of the acquired company is completely transferred to the acquiring company. |

| Financial Implications | In amalgamation, the assets and liabilities of the merging companies are combined to form the assets and liabilities of the new entity. | In absorption, the assets and liabilities of the acquired company become the assets and liabilities of the acquiring company. |

| Accounting Treatment | In amalgamation, the financial statements of the merging companies are combined to form the financial statements of the new entity. | In absorption, the financial statements of the acquired company are incorporated into the financial statements of the acquiring company. |

| Continuity of Business | In amalgamation, the businesses of the merging companies continue to operate as part of the new entity. | In absorption, the acquired company ceases to exist as a separate entity and its business becomes a part of the acquiring company’s operations. |

| Brand Identity | In amalgamation, the merging companies may choose to retain their individual brand identities or create a new brand identity for the new entity. | In absorption, the acquired company loses its brand identity and becomes a part of the acquiring company’s brand identity. |

| Shareholder Approval | In amalgamation, the merger requires approval from the shareholders of both merging companies. | In absorption, the acquiring company may acquire the shares of the acquired company without requiring shareholder approval. |

| Management Structure | In amalgamation, the management structure of the new entity may be a combination of the management structures of the merging companies. | In absorption, the acquired company’s management structure may be replaced by the acquiring company’s management structure. |

| Legal Process | Amalgamation requires a legal process to be followed, such as filing of documents with the Registrar of Companies. | Absorption also requires a legal process, such as obtaining necessary regulatory approvals and filing of documents with the Registrar of Companies. |

Examples of Amalgamation and Absorption

Amalgamation and absorption are two popular methods of corporate restructuring in India. Here are some examples of both:

Amalgamation:

1. HDFC Bank and Times Bank

In 2000, HDFC Bank acquired Times Bank through an amalgamation. The shareholders of Times Bank received HDFC Bank shares in exchange for their Times Bank shares. The new entity was named HDFC Bank Limited.

2. Vodafone and Idea Cellular

In 2018, Vodafone India and Idea Cellular merged through an amalgamation to create India’s largest telecom company, Vodafone Idea Limited. The shareholders of Idea Cellular received Vodafone India shares in exchange for their Idea Cellular shares.

Absorption:

1. Tata Steel and Bhushan Steel

In 2018, Tata Steel acquired Bhushan Steel through an absorption. Tata Steel gained control over Bhushan Steel’s assets and liabilities, and the shareholders of Bhushan Steel received payment for their shares in cash. The absorption helped Tata Steel become one of the leading steelmakers in India.

2. Hindalco and Novelis

In 2007, Hindalco Industries acquired Novelis, a Canadian company, through an absorption. Hindalco gained control over Novelis’ assets and liabilities, and the shareholders of Novelis received payment for their shares in cash and Hindalco shares. The absorption helped Hindalco become one of the world’s largest aluminium rolling companies.

Conclusion

While amalgamation and absorption may seem similar at first glance, there are key differences between the two. Amalgamation involves the combination of two or more companies to form a new entity, while absorption involves one company acquiring another and incorporating it into its own operations. The accounting treatment, legal aspects, control over assets and liabilities, and impact on shareholders can all vary between these two methods of combination. It’s important to carefully consider these differences when making business decisions involving mergers and acquisitions.

Important FAQs

What is the difference between amalgamation and absorption?

Amalgamation involves the combination of two or more companies to form a new entity, while absorption involves one company acquiring another and incorporating it into its own operations.

How do the accounting treatments differ between amalgamation and absorption?

In amalgamation, the acquired company’s assets and liabilities are recorded at their book value, while in absorption, they are recorded at their fair value.

What are the legal differences between amalgamation and absorption?

In amalgamation, the merging companies come together to form a new entity with its own legal identity, while in absorption, the acquired company ceases to exist as a separate legal entity and becomes part of the acquiring company.

Who gains control over assets and liabilities in amalgamation and absorption?

In amalgamation, the assets and liabilities of the merging companies are transferred to the new entity, while in absorption, the acquiring company gains control over the assets and liabilities of the acquired company.

In amalgamation, the shareholders of each company become shareholders of the new entity, while in absorption, the shareholders of the acquired company receive payment for their shares.