Contents

- 1 Introduction

- 2 Informal Sources of Credit

- 3 Differences between Formal and Informal Sources of Credit

- 4 Which Source of Credit is Right for You?

- 5 The Role of Credit History in Accessing Formal and Informal Sources of Credit

- 6 Summary

- 7 FAQs

- 7.1 What are formal sources of credit?

- 7.2 What are informal sources of credit?

- 7.3 What are the main differences between formal and informal sources of credit?

- 7.4 Why might someone choose to use informal sources of credit over formal sources?

- 7.5 What are some risks associated with using informal sources of credit?

- 7.6 How can someone determine which source of credit is best for their needs?

Learn about the key differences between formal and informal sources of credit. Discover how these two types of credit differ in terms of accessibility, interest rates, and repayment options, and learn which one may be the best fit for your financial needs. Whether you’re looking to borrow money for personal or business use, understanding the pros and cons of formal and informal credit can help you make an informed decision.

Introduction

Credit is an essential concept of modern finance, and it refers to the ability of an individual or business to borrow money with the promise of repaying it in the future. Access to credit is vital for economic growth and development, as it enables individuals and businesses to invest in their future by purchasing homes, cars, or funding their education or business ventures. Credit is usually obtained from two primary sources, formal and informal sources of credit.

Formal Sources of Credit

Formal sources of credit refer to established financial institutions that provide credit services to individuals and businesses. Examples of formal sources of credit include banks, credit unions, and microfinance institutions.

Formal sources of credit typically require individuals and businesses to meet specific documentation requirements before accessing credit services. This may include providing proof of income, collateral, and a good credit score. Formal sources of credit are also regulated by government agencies, ensuring that they adhere to specific lending regulations.

Advantages of Formal Sources of Credit

One of the main advantages of formal sources of credit is that they usually have lower interest rates compared to informal sources of credit. Formal sources of credit also offer flexible repayment terms, making it easier for individuals and businesses to manage their debt.

Disadvantages of Formal Sources of Credit

One of the significant drawbacks of formal sources of credit is that they can be challenging to access, especially for individuals and businesses with a poor credit score. Additionally, formal sources of credit may require collateral, making it difficult for individuals and businesses without assets to obtain credit.

Informal Sources of Credit

Informal sources of credit indicates lending practices that occur outside the formal financial system. Examples of informal sources of credit include friends and family, moneylenders, and pawnshops. Informal sources of credit are often characterized by fewer regulations and less stringent documentation requirements.

Advantages of Informal Sources of Credit

One of the main advantages of informal sources of credit is that they are accessible to individuals and businesses that may not qualify for formal sources of credit. Informal sources of credit also have flexible repayment terms, and they can offer credit to individuals and businesses without collateral.

Disadvantages of Informal Sources of Credit

One of the significant drawbacks of informal sources of credit is that they often have higher interest rates compared to formal sources of credit. Informal sources of credit can also be risky, as they are not regulated, and the terms of the loan may be unclear.

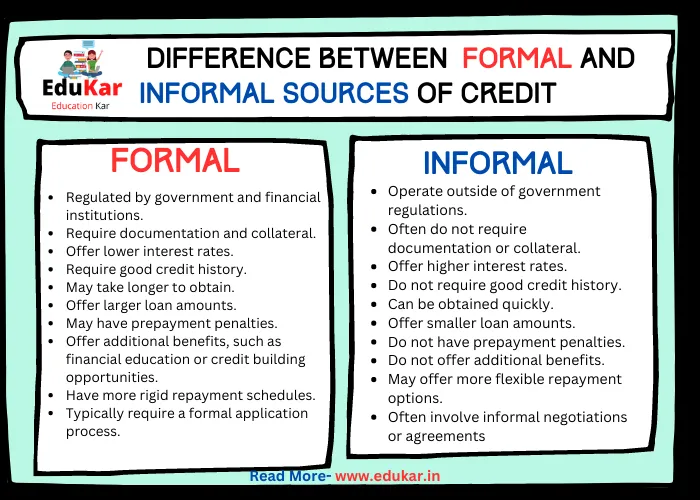

Differences between Formal and Informal Sources of Credit

| Formal Sources of Credit | Informal Sources of Credit |

|---|---|

| Regulated by government and financial institutions | Operate outside of government regulations |

| Require documentation and collateral | Often do not require documentation or collateral |

| Offer lower interest rates | Offer higher interest rates |

| Require good credit history | Do not require good credit history |

| May take longer to obtain | Can be obtained quickly |

| Offer larger loan amounts | Offer smaller loan amounts |

| May have prepayment penalties | Do not have prepayment penalties |

| May offer additional benefits, such as financial education or credit building opportunities | Do not offer additional benefits |

| May have more rigid repayment schedules | May offer more flexible repayment options |

| Typically require a formal application process | Often involve informal negotiations or agreements |

Which Source of Credit is Right for You?

Choosing a source of credit depends on several factors, such as the purpose of the loan, credit history, and repayment ability. Individuals and businesses with a good credit score and collateral may find it easier to access formal sources of credit, while those without collateral or a poor credit score may opt for informal sources of credit. Additionally, the purpose of the loan may influence the choice of credit.

For instance, individuals and businesses may opt for formal sources of credit when purchasing a home or a car, while informal sources of credit may be more suitable for short-term loans.

The Role of Credit History in Accessing Formal and Informal Sources of Credit

Credit history is an essential factor that lenders consider when deciding whether to grant a loan. A good credit score makes it easier for individuals and businesses to access formal sources of credit, while a poor credit score may limit access to formal sources of credit. On the other hand, informal sources of credit may not consider credit history when granting loans, making them more accessible to individuals and businesses with a poor credit score.

Summary

Formal and informal sources of credit play a crucial role in the financial system, and individuals and businesses need to understand the differences between the two sources before choosing a source of credit. Formal sources of credit offer lower interest rates and flexible repayment terms, but they can be challenging to access, especially for individuals and businesses with a poor credit score. Informal sources of credit are more accessible but often come with higher interest rates and unclear repayment terms. Ultimately, the choice of credit depends on the individual or business’s financial situation and the purpose of the loan.

FAQs

What are formal sources of credit?

Formal sources of credit are institutions that are recognized and regulated by the government, such as banks, credit unions, and other financial institutions.

What are informal sources of credit?

Informal sources of credit are non-regulated sources of credit, such as moneylenders, friends and family, and other non-institutional sources.

What are the main differences between formal and informal sources of credit?

Formal sources of credit are regulated by the government and follow established guidelines and procedures, while informal sources of credit do not have any such regulations or guidelines. Formal sources of credit also typically charge lower interest rates than informal sources, but the process of obtaining credit from formal sources is generally more time-consuming and requires more paperwork.

Why might someone choose to use informal sources of credit over formal sources?

Some people may prefer to use informal sources of credit because they have difficulty obtaining credit from formal sources due to poor credit history, lack of collateral, or other factors. Informal sources may also offer more flexible repayment terms than formal sources.

What are some risks associated with using informal sources of credit?

Informal sources of credit often charge higher interest rates than formal sources, which can lead to a cycle of debt if the borrower is unable to repay the loan. Additionally, because informal sources are not regulated, there is a risk of fraud or predatory lending practices.

How can someone determine which source of credit is best for their needs?

The best source of credit for an individual will depend on their specific financial situation and needs. It is important to consider factors such as interest rates, repayment terms, and any associated fees before choosing a source of credit. It may be helpful to speak with a financial advisor or credit counselor to determine the best course of action.