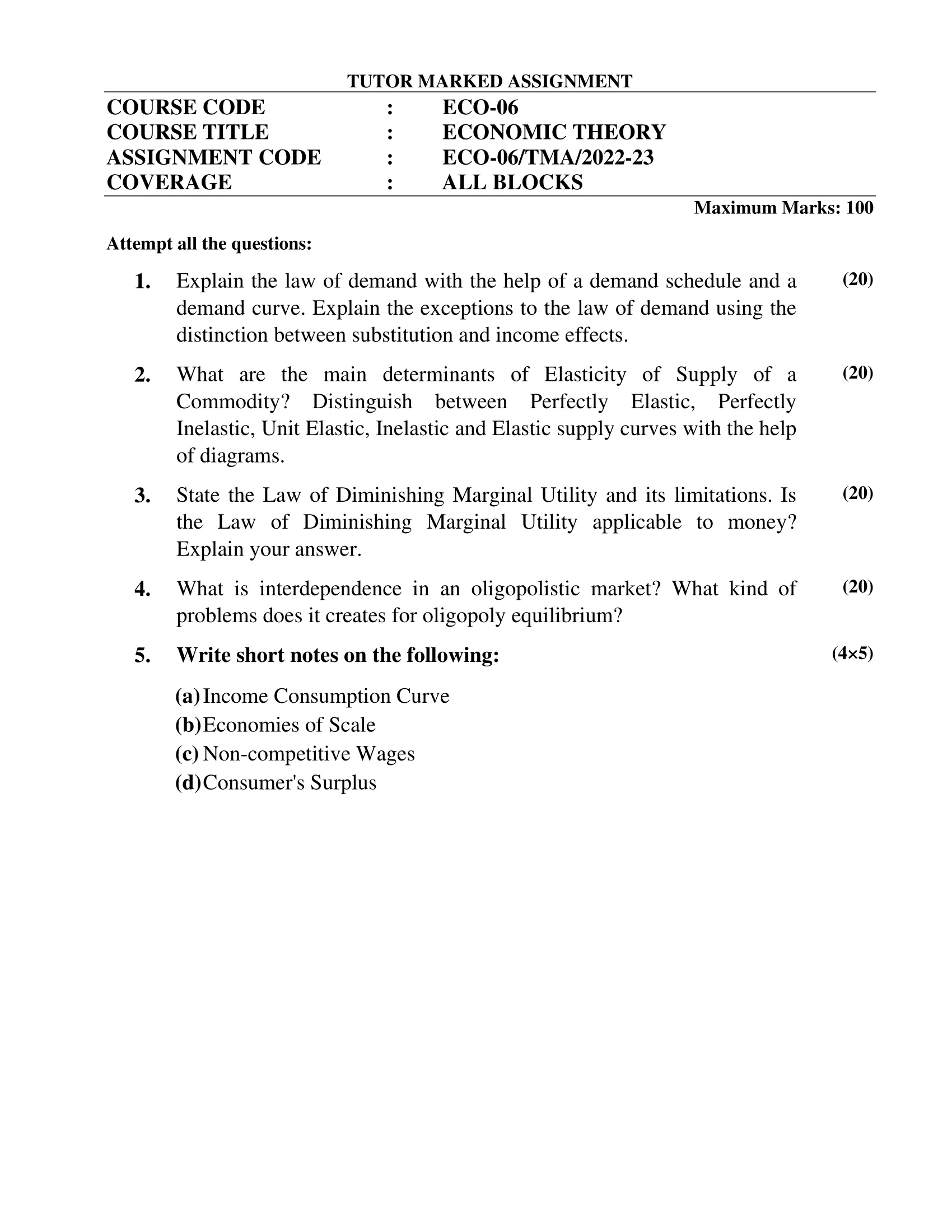

Contents

- 1 1. Explain the law of demand with the help of a demand schedule and a demand curve. Explain the exceptions to the law of demand using the distinction between substitution and income effects.

- 2 2. What are the main determinants of Elasticity of Supply of a Commodity? Distinguish between Perfectly Elastic, Perfectly Inelastic, Unit Elastic, Inelastic and Elastic supply curves with the help of diagrams.

- 3 3. State the Law of Diminishing Marginal Utility and its limitations. Is the Law of Diminishing Marginal Utility applicable to money? Explain your answer.

- 4 4. What is interdependence in an oligopolistic market? What kind of problems does it creates for oligopoly equilibrium?

- 5 5. Write short notes on the following:

- 6 (a) Income Consumption Curve

- 7 (b) Economies of Scale

- 8 (c) Non-competitive Wages

- 9 (d) Consumer’s Surplus

| Title | ECO-06: IGNOU B.Com Solved Assignment 2022-2023 |

| University | IGNOU |

| Degree | Bachelor Degree Programme |

| Course Code | ECO-06 |

| Course Name | ECONOMIC THEORY |

| Programme Name | B.Com |

| Programme Code | BDP |

| Total Marks | 100 |

| Year | 2022-2023 |

| Language | English |

| Assignment Code | ECO-06/TMA/2022-23 |

| Assignment PDF | Click Here |

| Last Date for Submission of Assignment: | For June Examination: 31st April For December Examination: 30th September |

1. Explain the law of demand with the help of a demand schedule and a demand curve. Explain the exceptions to the law of demand using the distinction between substitution and income effects.

Ans: The law of demand is a fundamental principle in economics that states that as the price of a good or service increases, the quantity demanded of that good or service decreases, all other things being equal. Conversely, as the price of a good or service decreases, the quantity demanded of that good or service increases, all other things being equal.

A demand schedule is a table that shows the quantity of a good or service that consumers are willing and able to buy at different prices, while a demand curve is a graphical representation of the same information.

Here is an example demand schedule for apples:

| Price per apple ($) | Quantity demanded (apples) |

|---|---|

| 1 | 10 |

| 2 | 8 |

| 3 | 6 |

| 4 | 4 |

| 5 | 2 |

As you can see, as the price of apples increases, the quantity demanded of apples decreases. This relationship between price and quantity demanded is known as the law of demand.

However, there are certain exceptions to the law of demand. One of the most important exceptions is known as the Giffen good, which is a good that people consume more of as its price rises. This seems to contradict the law of demand, but it can be explained by the fact that some goods are so important to consumers that they consume more of them even as their prices rise. This effect is known as the income effect, and it can sometimes overpower the substitution effect (where consumers switch to cheaper alternatives when the price of a good rises).

Another exception to the law of demand is the Veblen good, which is a luxury good that people consume more of as its price rises because they view it as a status symbol. This effect is also due to the income effect, as people with higher incomes can afford to buy more of these goods even as their prices rise.

2. What are the main determinants of Elasticity of Supply of a Commodity? Distinguish between Perfectly Elastic, Perfectly Inelastic, Unit Elastic, Inelastic and Elastic supply curves with the help of diagrams.

Ans: The elasticity of supply of a commodity refers to the responsiveness of the quantity supplied of that commodity to changes in its price. It is determined by a number of factors, including:

- Time: The elasticity of supply tends to be more elastic in the long run, as producers have more time to adjust their production levels in response to changes in price.

- Availability of inputs: If the inputs required to produce a commodity are readily available, then the elasticity of supply will be higher. Conversely, if the inputs are scarce or difficult to obtain, then the elasticity of supply will be lower.

- Ease of production: If it is easy and inexpensive to produce a commodity, then the elasticity of supply will be higher. If it is difficult or expensive to produce, then the elasticity of supply will be lower.

- Flexibility of production: If producers can easily switch between producing one commodity and another, then the elasticity of supply will be higher. If production is specialized and cannot be easily switched, then the elasticity of supply will be lower.

The following are the different types of supply curves, each representing a different level of elasticity of supply:

- Perfectly elastic supply curve: A perfectly elastic supply curve is a horizontal line, indicating that any increase or decrease in price will result in an infinite increase or decrease in the quantity supplied. This occurs when producers can increase production without any increase in cost.

- Perfectly inelastic supply curve: A perfectly inelastic supply curve is a vertical line, indicating that the quantity supplied is fixed and does not respond to changes in price. This occurs when the commodity can only be produced in limited quantities or when there are no substitutes for the commodity.

- Unit elastic supply curve: A unit elastic supply curve is a diagonal line, indicating that the percentage change in price is equal to the percentage change in quantity supplied. This occurs when the percentage change in price is exactly offset by a proportionate change in quantity supplied.

- Inelastic supply curve: An inelastic supply curve is a steeply sloping line, indicating that a change in price results in a relatively small change in quantity supplied. This occurs when producers cannot easily increase production in response to a price increase or decrease.

- Elastic supply curve: An elastic supply curve is a gently sloping line, indicating that a change in price results in a relatively large change in quantity supplied. This occurs when producers can easily increase or decrease production in response to a price change.

3. State the Law of Diminishing Marginal Utility and its limitations. Is the Law of Diminishing Marginal Utility applicable to money? Explain your answer.

Ans: The Law of Diminishing Marginal Utility states that as a consumer consumes more and more units of a particular good or service, the marginal utility or satisfaction obtained from each additional unit will decrease, assuming all other factors remain constant. This means that the more of a good or service a person consumes, the less additional satisfaction they will derive from each additional unit.

The limitations of the Law of Diminishing Marginal Utility include the following:

- The law assumes that all other factors remain constant, which is often not the case in the real world. For example, a consumer’s preferences or income may change, affecting their level of satisfaction.

- The law only applies to goods or services that are consumed in small amounts. For goods or services that are consumed in large quantities, the law may not hold true.

- The law assumes that the consumer is rational and has perfect knowledge of the goods and services being consumed, which may not always be the case.

Regarding the question of whether the Law of Diminishing Marginal Utility is applicable to money, the answer is somewhat debated among economists. Some argue that the law can apply to money, as the satisfaction derived from an additional unit of money may decrease as a person’s income increases. For example, a person may derive greater satisfaction from receiving a $100 bonus when their income is $1,000 per month, compared to receiving the same $100 bonus when their income is $10,000 per month.

However, others argue that the law does not apply to money, as money is not a good or service that is consumed for its own sake. Rather, money is simply a means of obtaining goods and services, and the satisfaction derived from it is based on the goods and services it can purchase. As such, the satisfaction derived from money is not subject to the same diminishing returns as goods and services themselves.

4. What is interdependence in an oligopolistic market? What kind of problems does it creates for oligopoly equilibrium?

Ans: Interdependence in an oligopolistic market refers to the mutual influence and strategic behavior of firms in response to the actions of their rivals. In an oligopoly, a small number of firms dominate the market, and each firm’s pricing and output decisions can have a significant impact on the market as a whole. This means that firms must consider the likely responses of their competitors when making decisions about pricing, advertising, product differentiation, and other strategic factors.

Interdependence creates a number of problems for oligopoly equilibrium, including:

- Uncertainty: In an oligopoly, firms cannot predict the actions of their competitors with certainty. This leads to uncertainty about the likely outcomes of any particular decision, and can make it difficult for firms to make optimal decisions.

- Strategic interactions: Firms in an oligopoly must take into account the strategic interactions with their rivals. The actions of one firm can have a significant impact on the actions of its competitors, and vice versa. This can lead to complex strategic interactions, which can be difficult to predict and analyze.

- Price rigidity: Oligopoly markets often exhibit price rigidity, meaning that prices do not adjust quickly to changes in supply and demand. This can result in prices remaining high even when there is excess supply, or remaining low even when there is excess demand.

- Inefficiency: Interdependence can lead to inefficiencies in oligopoly markets, such as overproduction, underproduction, or excessive advertising. This can result in higher costs and lower profits for firms, as well as reduced consumer welfare.

5. Write short notes on the following:

(a) Income Consumption Curve

Ans: The income consumption curve is a graphical representation of the relationship between income and consumption of goods and services. It shows how a consumer’s consumption changes as their income changes, assuming all other factors remain constant, such as the price of goods and services.

The curve is typically drawn with consumption on the vertical axis and income on the horizontal axis. As income increases, the curve shows that consumption also increases, but at a decreasing rate. This is because as income increases, the consumer tends to spend a smaller proportion of their income on basic necessities and more on luxury goods.

The income consumption curve is useful in understanding consumer behavior and can be used by businesses and policymakers to predict how changes in income will affect consumption patterns. It is also a key tool in the study of economics, particularly in the field of microeconomics.

(b) Economies of Scale

Ans: Economies of scale refer to the cost advantages that a business can achieve as it increases its output or scale of production. In other words, as a firm produces more units of a product, the cost of producing each unit tends to decrease.

There are two main types of economies of scale: internal and external. Internal economies of scale arise from factors within the firm, such as specialization of labor, bulk buying of raw materials, and improved technology. External economies of scale, on the other hand, come from external factors such as improvements in infrastructure, access to a skilled workforce, and knowledge spillovers.

Economies of scale can lead to several benefits for a firm, such as increased efficiency, lower costs per unit of output, increased market share, and higher profitability. However, there are also some potential drawbacks to economies of scale, such as reduced flexibility, increased bureaucracy, and decreased innovation.

(c) Non-competitive Wages

Ans: Non-competitive wages refer to wages that are not determined by the supply and demand of labor in a competitive labor market. In other words, they are wages that are set by factors other than the market forces of supply and demand.

One example of non-competitive wages is a minimum wage, which is a legal requirement that employers pay a certain minimum wage to their workers. Other examples include collective bargaining agreements, where wages are negotiated between unions and employers, and government-mandated wage scales for certain occupations.

Non-competitive wages can have both positive and negative effects on the labor market. On the one hand, they can help to ensure that workers receive a fair wage and that certain basic labor standards are met. On the other hand, they can lead to market distortions, such as higher unemployment rates, reduced labor force participation, and reduced competitiveness of firms.

In addition, non-competitive wages can have distributional effects, as they may benefit certain groups of workers more than others. For example, a minimum wage may disproportionately benefit low-skilled workers but may also lead to reduced employment opportunities for these workers.

(d) Consumer’s Surplus

Ans: Consumer’s surplus refers to the difference between the price that a consumer is willing to pay for a good or service and the actual price that they pay. In other words, it is the amount of value that a consumer gains from purchasing a good or service above and beyond what they actually paid for it.

Consumer’s surplus is a concept that is used in microeconomics to measure the welfare or benefit that consumers receive from a particular market transaction. It is typically represented graphically as the area between the demand curve and the price paid for the good or service.

For example, if a consumer is willing to pay $10 for a product but only has to pay $8 to purchase it, they experience a consumer’s surplus of $2. This means that the consumer has gained $2 worth of additional value from the transaction.

Consumer’s surplus is an important concept for understanding consumer behavior and market efficiency. It can be used to measure the overall welfare of consumers in a particular market, and can be used by policymakers to determine the optimal level of production and consumption of goods and services.

How to Download ECO-06 Solved Assignment?

You can download it from the www.edukar.in, they have a big database for all the IGNOU solved assignments.

Is the ECO-06 Solved Assignment Free?

Yes this is absolutely free to download the solved assignment from www.edukar.in

What is the last submission date for ECO-06 Solved Assignment?

For June Examination: 31st April, For December Examination: 30th October