Contents

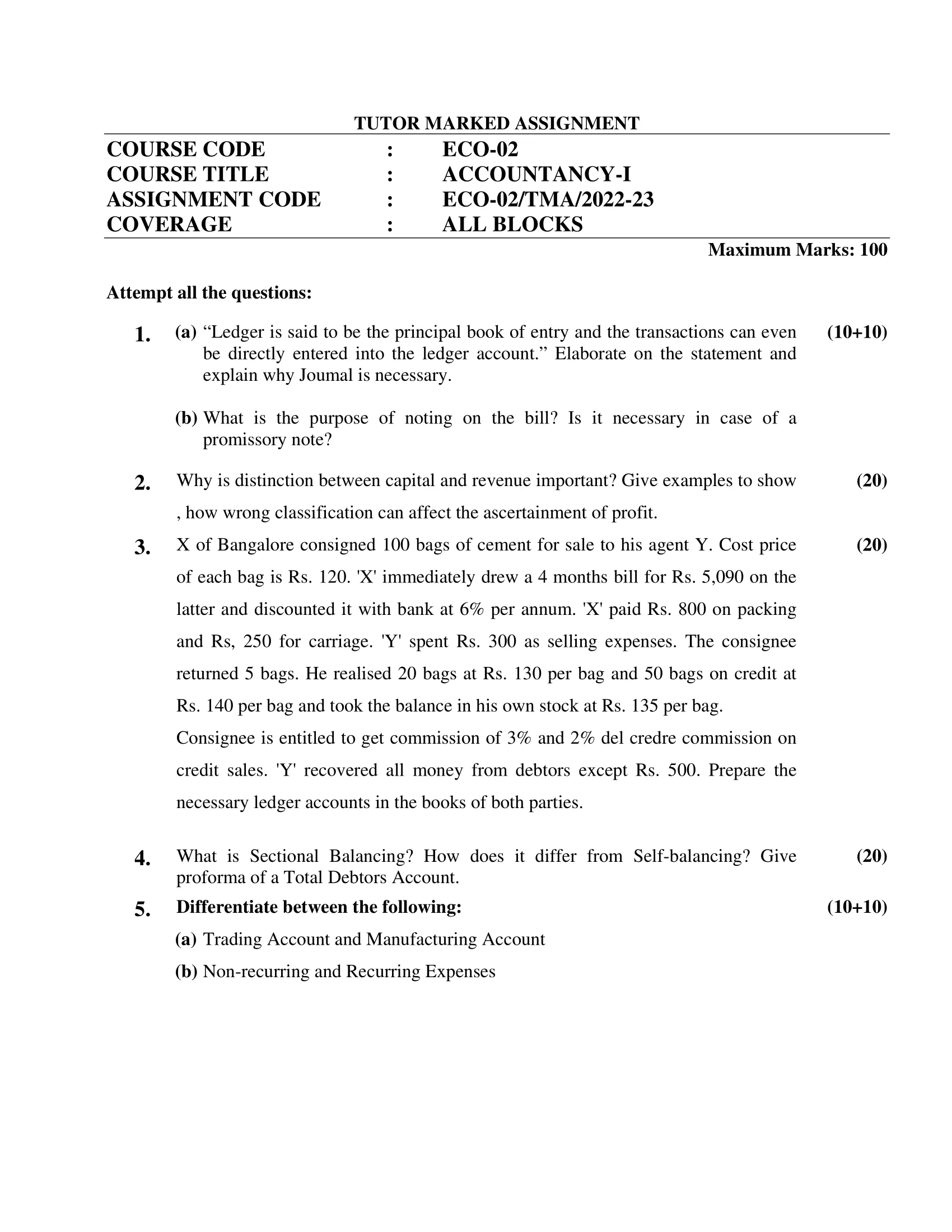

- 1 1. (a) “Ledger is said to be the principal book of entry and the transactions can even be directly entered into the ledger account.” Elaborate on the statement and explain why Joumal is necessary.

- 2 (b) What is the purpose of noting on the bill? Is it necessary in case of a promissory note?

- 3 2. Why is distinction between capital and revenue important? Give examples to show , how wrong classification can affect the ascertainment of profit.

- 4 3. X of Bangalore consigned 100 bags of cement for sale to his agent Y. Cost price of each bag is Rs. 120. ‘X’ immediately drew a 4 months bill for Rs. 5,090 on the latter and discounted it with bank at 6% per annum. ‘X’ paid Rs. 800 on packing and Rs, 250 for carriage. ‘Y’ spent Rs. 300 as selling expenses. The consignee returned 5 bags. He realised 20 bags at Rs. 130 per bag and 50 bags on credit at Rs. 140 per bag and took the balance in his own stock at Rs. 135 per bag. Consignee is entitled to get commission of 3% and 2% del credre commission on credit sales. ‘Y’ recovered all money from debtors except Rs. 500. Prepare the necessary ledger accounts in the books of both parties.

- 5 4. What is Sectional Balancing? How does it differ from Self-balancing? Give proforma of a Total Debtors Account.

- 6 5. Differentiate between the following:

- 7 (a) Trading Account and Manufacturing Account

- 8 (b) Non-recurring and Recurring Expenses

| Title | ECO-02: IGNOU B.Com Solved Assignment 2022-2023 |

| University | IGNOU |

| Degree | Bachelor Degree Programme |

| Course Code | ECO-02 |

| Course Name | Accountancy-1 |

| Programme Name | B.Com |

| Programme Code | BDP |

| Total Marks | 100 |

| Year | 2022-2023 |

| Language | English |

| Assignment Code | ECO-02/TMA/2022-23 |

| Assignment PDF | Click Here |

| Last Date for Submission of Assignment: | For June Examination: 31st April For December Examination: 30th September |

1. (a) “Ledger is said to be the principal book of entry and the transactions can even be directly entered into the ledger account.” Elaborate on the statement and explain why Joumal is necessary.

Ans: In accounting, the ledger is the principal book of entry where all the transactions of a business are recorded in a chronological order. It is also known as the book of final entry because all the information recorded in the journal is posted to the ledger accounts. The ledger provides a summary of all the transactions and balances in each account, making it easier for accountants to prepare financial statements.

One of the advantages of using a ledger is that transactions can be directly entered into the appropriate account, eliminating the need for a separate journal. This method is known as the direct posting system, and it allows accountants to save time and reduce the risk of errors that may occur during the transfer of information from one book to another.

However, despite the convenience of the direct posting system, a journal is still necessary in accounting. The journal is used to record transactions that cannot be directly posted to the ledger, such as adjusting entries and closing entries. Additionally, the journal serves as a record of original entry, providing a complete and chronological record of all transactions.

Furthermore, the journal also allows for proper documentation and supporting details of the transactions, which can be helpful in case of audits or disputes. Without a journal, it may be difficult to trace the source of a transaction or to identify errors in the accounting process.

(b) What is the purpose of noting on the bill? Is it necessary in case of a promissory note?

Ans: Noting on a bill of exchange refers to the process of recording on the bill any information about its presentment, acceptance, or non-acceptance, as well as any other details relevant to the transaction. The purpose of noting is to create a record of the transaction and any actions taken by the parties involved, which can be used as evidence in case of disputes or legal action.

Noting is especially important in case of a promissory note, which is a type of bill of exchange that contains a promise to pay a certain amount of money on a specific date or on demand. If the promissory note is not paid on the due date, noting can be used to show that it was presented for payment and not paid, which can be used as evidence in legal proceedings to recover the amount owed.

In addition, noting on a promissory note can also serve as a reminder to the parties involved of the payment due date and any actions that need to be taken to ensure timely payment. It can also help to prevent disputes or misunderstandings by providing a clear record of the transaction.

Therefore, noting on a bill of exchange, including a promissory note, is an important practice that can help to ensure the accuracy and validity of financial transactions and protect the rights of the parties involved.

2. Why is distinction between capital and revenue important? Give examples to show , how wrong classification can affect the ascertainment of profit.

Ans: The distinction between capital and revenue is essential in accounting because it helps to ensure that the financial statements reflect the true financial position and performance of a business. Capital refers to the funds invested in a business, while revenue refers to the income generated from the operations of the business.

Incorrect classification of capital and revenue items can affect the ascertainment of profit in several ways. Here are some examples:

- Capital Expenditures Treated as Revenue Expenditures: If a capital expenditure is wrongly classified as a revenue expenditure, the profit of the business will be overstated. Capital expenditures are investments in the long-term assets of a business, such as land, buildings, and equipment. These assets are expected to provide benefits to the business for many years, so their cost is spread over their useful life through depreciation. On the other hand, revenue expenditures are expenses incurred to maintain the day-to-day operations of a business, such as salaries, rent, and utilities. If a capital expenditure is treated as a revenue expenditure, its cost will be fully expensed in the current period, which will reduce the profit for that period. Conversely, if a revenue expenditure is treated as a capital expenditure, it will overstate the profit for the period.

- Revenue Items Treated as Capital Items: If a revenue item is wrongly classified as a capital item, the profit of the business will be understated. Revenue items are income generated from the operations of a business, such as sales revenue and interest income. These items are recognized in the income statement in the period in which they are earned. On the other hand, capital items are non-operating items, such as gains on the sale of assets and investments. If a revenue item is treated as a capital item, it will not be recognized in the income statement, which will understate the profit for the period.

- Non-Recurring Items Treated as Recurring Items: If non-recurring items, such as gains or losses on the sale of fixed assets, are treated as recurring items, the profit of the business will be distorted. Non-recurring items are one-time events that do not represent the ongoing operations of the business. If they are treated as recurring items, the profit for the period will not reflect the true performance of the business.

3. X of Bangalore consigned 100 bags of cement for sale to his agent Y. Cost price of each bag is Rs. 120. ‘X’ immediately drew a 4 months bill for Rs. 5,090 on the latter and discounted it with bank at 6% per annum. ‘X’ paid Rs. 800 on packing and Rs, 250 for carriage. ‘Y’ spent Rs. 300 as selling expenses. The consignee returned 5 bags. He realised 20 bags at Rs. 130 per bag and 50 bags on credit at Rs. 140 per bag and took the balance in his own stock at Rs. 135 per bag. Consignee is entitled to get commission of 3% and 2% del credre commission on credit sales. ‘Y’ recovered all money from debtors except Rs. 500. Prepare the necessary ledger accounts in the books of both parties.

Ans:

4. What is Sectional Balancing? How does it differ from Self-balancing? Give proforma of a Total Debtors Account.

Ans: Sectional balancing is a method of balancing ledger accounts by dividing them into sections based on the nature or type of transactions. Each section is then balanced separately to ensure accuracy and to make the process of identifying errors easier. This method is commonly used for accounts with a large volume of transactions, such as sales and purchases accounts.

On the other hand, self-balancing is a method of balancing ledger accounts where the debit and credit entries are recorded in the same account, resulting in the account always being in balance. This method is used for accounts that are frequently updated, such as cash and bank accounts.

Here’s a proforma of a total debtors account:

Total Debtors Account

| Date | Particulars | Invoice No. | Debit (Rs.) | Credit (Rs.) | Balance (Rs.) |

|---|---|---|---|---|---|

| 01/01/2022 | Balance b/d | 50,000 | 50,000 | ||

| 15/01/2022 | Sales | INV-001 | 20,000 | 30,000 | |

| 20/01/2022 | Sales | INV-002 | 15,000 | 15,000 | |

| 25/01/2022 | Sales Return | SR-001 | 5,000 | 20,000 | |

| 31/01/2022 | Receipt | RCPT-001 | 10,000 | 30,000 | |

| 15/02/2022 | Sales | INV-003 | 25,000 | 5,000 | |

| 28/02/2022 | Receipt | RCPT-002 | 5,000 | 10,000 | |

| 31/03/2022 | Balance c/d | 10,000 | 10,000 | ||

| Total | 70,000 | 70,000 |

So, in the above proforma, the total debtors account is divided into different sections based on the type of transaction such as sales, sales return, and receipts. The account is balanced by calculating the debit and credit balances for each section and then transferring the balances to the total column. The final balance of the account is the difference between the total debits and total credits, which in this case is Rs. 10,000.

5. Differentiate between the following:

(a) Trading Account and Manufacturing Account

Ans: A trading account and manufacturing account are two types of financial accounts used in accounting to determine the cost of goods sold and calculate the gross profit of a business. However, there are some key differences between the two:

- Definition: A trading account is an account that shows the gross profit or loss of a business that trades in goods. On the other hand, a manufacturing account is an account that shows the cost of goods produced by a manufacturing business.

- Nature of Business: Trading account is suitable for a business that deals with buying and selling of goods, whereas the manufacturing account is suitable for businesses that manufacture goods.

- Expenses: The trading account only includes direct expenses, such as cost of goods sold, carriage inward, and customs duty, while the manufacturing account includes direct and indirect expenses, such as raw materials, factory rent, electricity, and salaries.

- Calculation of Gross Profit: In a trading account, the gross profit is calculated as the difference between the cost of goods sold and the sales revenue. In a manufacturing account, the gross profit is calculated as the difference between the cost of goods produced and the sales revenue.

- Inventory valuation: The trading account values the inventory at cost or net realizable value, whichever is lower, while the manufacturing account values inventory at the cost of raw materials, direct labor, and manufacturing overheads.

(b) Non-recurring and Recurring Expenses

Ans: Non-recurring expenses and recurring expenses are two types of expenses that businesses incur. The main differences between them are:

- Definition: Recurring expenses are regular expenses that a business incurs on a frequent basis, such as monthly or annually. Non-recurring expenses, on the other hand, are one-time or occasional expenses that a business incurs.

- Frequency: Recurring expenses occur on a regular basis, whereas non-recurring expenses happen less frequently, usually only once.

- Predictability: Recurring expenses are predictable as they are part of the regular operations of the business, and their occurrence can be anticipated. Non-recurring expenses are often unexpected, and their timing and amount are not easily predictable.

- Budgeting: Recurring expenses are usually budgeted for in advance, and the business can plan for them. Non-recurring expenses are typically not budgeted for, and the business must find ways to fund them when they occur.

- Examples: Examples of recurring expenses include rent, salaries, utilities, and insurance premiums. Examples of non-recurring expenses include equipment purchases, repairs, legal fees, and marketing campaigns.

How to Download ECO-02 Solved Assignment?

You can download it from the www.edukar.in, they have a big database for all the IGNOU solved assignments.

Is the ECO-02 Solved Assignment Free?

Yes this is absolutely free to download the solved assignment from www.edukar.in

What is the last submission date for ECO-02 Solved Assignment?

For June Examination: 31st April, For December Examination: 30th October

")