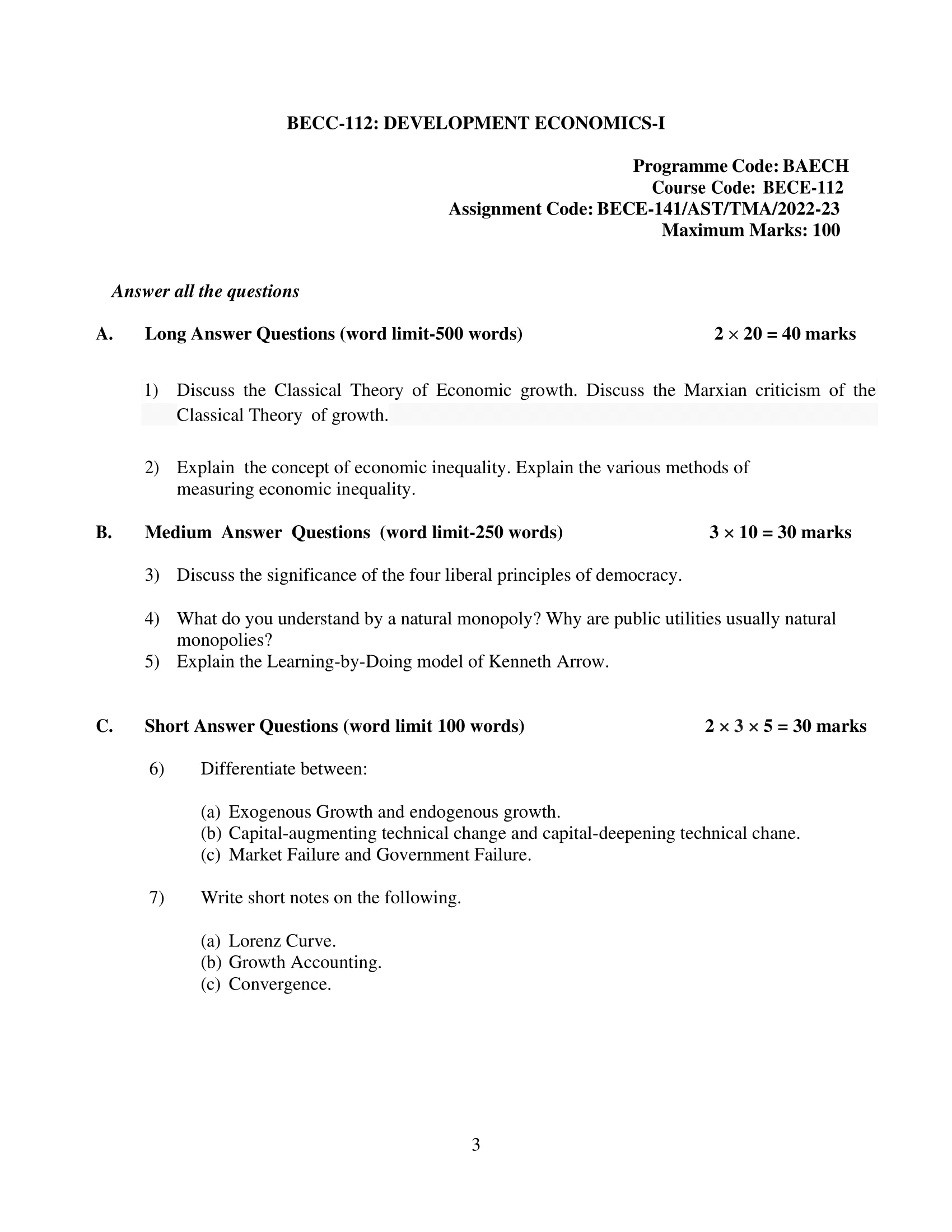

Contents

- 1 A. Long Answer Questions (word limit-500 words)

- 2 1) Discuss the Classical Theory of Economic growth. Discuss the Marxian criticism of the Classical Theory of growth.

- 3 2) Explain the concept of economic inequality. Explain the various methods of measuring economic inequality.

- 4 B. Medium Answer Questions (word limit-250 words)

- 5 3) Discuss the significance of the four liberal principles of democracy.

- 6 4) What do you understand by a natural monopoly? Why are public utilities usually natural monopolies?

- 7 5) Explain the Learning-by-Doing model of Kenneth Arrow.

- 8 C. Short Answer Questions (word limit 100 words)

- 9 6) Differentiate between:

- 10 (a) Exogenous Growth and endogenous growth.

- 11 (b) Capital-augmenting technical change and capital-deepening technical chane.

- 12 (c) Market Failure and Government Failure.

- 13 7) Write short notes on the following.

- 14 (a) Lorenz Curve.

- 15 (b) Growth Accounting.

- 16 (c) Convergence.

| Title | BECC-112: IGNOU BAG Solved Assignment 2022-2023 |

| University | IGNOU |

| Degree | Bachelor Degree Programme |

| Course Code | BECC-112 |

| Course Name | DEVELOPMENT ECONOMICS-I |

| Programme Name | Bachelor of Arts (General) |

| Programme Code | BAG |

| Total Marks | 100 |

| Year | 2022-2023 |

| Language | English |

| Assignment Code | BECE-141/AST/TMA/2022-23 |

| Last Date for Submission of Assignment: | For June Examination: 31st April For December Examination: 30th September |

A. Long Answer Questions (word limit-500 words)

1) Discuss the Classical Theory of Economic growth. Discuss the Marxian criticism of the Classical Theory of growth.

Ans: The Classical Theory of Economic Growth, also known as the neoclassical growth theory, was developed by economists like Robert Solow and Trevor Swan in the mid-20th century. This theory attempts to explain how an economy can grow over time by increasing its production of goods and services.

The Classical Theory of Economic Growth assumes that an economy’s growth is driven by three factors: capital accumulation, labor force growth, and technological progress. Capital accumulation refers to the growth of the economy’s stock of physical capital, such as buildings, machinery, and equipment. Labor force growth refers to the growth of the population, and technological progress refers to the development of new and more efficient production techniques and methods.

According to the Classical Theory of Economic Growth, these three factors can increase an economy’s output and income in the long run. The theory suggests that an economy will experience diminishing returns to capital accumulation, meaning that each additional unit of capital added to the economy will provide a smaller increase in output. This implies that an economy can only grow sustainably if it invests in new technologies and improves its production methods.

However, the Marxian criticism of the Classical Theory of growth suggests that the theory has some flaws. Marx argued that the capitalist mode of production is inherently unstable and crisis-prone. According to Marx, capitalism is characterized by a tendency towards overproduction and underconsumption, which can lead to economic crises and depressions.

Marx also argued that the accumulation of capital in a capitalist economy leads to the exploitation of the working class. He suggested that capitalists extract surplus value from the labor of workers, which creates a class struggle between the owners of capital and the working class. Marx believed that this class struggle would eventually lead to the overthrow of the capitalist system and the establishment of a socialist society.

Moreover, Marx criticized the Classical Theory of Economic Growth for ignoring the environmental and social costs of economic growth. He argued that economic growth under capitalism would lead to the depletion of natural resources, environmental degradation, and social inequality.

2) Explain the concept of economic inequality. Explain the various methods of measuring economic inequality.

Ans: Economic inequality refers to the unequal distribution of income, wealth, and economic opportunities among individuals or households within a society. Inequality can arise from various factors, including differences in education, skills, labor market conditions, social and economic policies, and social identity characteristics such as race and gender.

Measuring economic inequality is important for policymakers and researchers to understand the extent and nature of inequality, identify its causes and consequences, and design effective policies to reduce it. Here are some methods of measuring economic inequality:

- Gini coefficient: The Gini coefficient is a widely used measure of income or wealth inequality that ranges from 0 to 1. A Gini coefficient of 0 indicates perfect equality, where everyone in a society has the same income or wealth. A Gini coefficient of 1 indicates perfect inequality, where one person or group has all the income or wealth, and everyone else has none. The Gini coefficient is calculated by plotting the cumulative share of income or wealth against the cumulative share of the population and measuring the area between the two curves.

- Theil index: The Theil index is a measure of economic inequality that considers the distribution of income or wealth among groups, as well as the overall distribution. It is based on the concept of entropy, which measures the degree of uncertainty or disorder in a system. The Theil index ranges from 0 to infinity, with higher values indicating higher levels of inequality.

- Palma ratio: The Palma ratio is a measure of income inequality that compares the share of income received by the top 10% of the population to the share received by the bottom 40% of the population. The Palma ratio is particularly useful for analyzing income inequality in developing countries, where income data may be less accurate.

- Coefficient of variation: The coefficient of variation is a measure of income or wealth inequality that compares the standard deviation of income or wealth to the mean. A higher coefficient of variation indicates higher levels of inequality.

- Atkinson index: The Atkinson index is a measure of inequality that takes into account the societal value of redistribution. The Atkinson index is based on the idea that people care not only about their own income but also about the income of others. The Atkinson index ranges from 0 to 1, with higher values indicating higher levels of inequality.

B. Medium Answer Questions (word limit-250 words)

3) Discuss the significance of the four liberal principles of democracy.

Ans: The four liberal principles of democracy are a crucial foundation for modern democratic societies. These principles include individual rights and freedoms, the rule of law, a market-based economy, and representative government.

Individual rights and freedoms refer to the belief that individuals have inherent rights that should be protected by the government. These include rights such as freedom of speech, religion, and assembly. This principle is essential for protecting the dignity and autonomy of citizens and preventing the abuse of power by the state.

The rule of law means that everyone, including the government, is subject to the law. This principle ensures that government actions are constrained by legal limits, preventing arbitrary and capricious exercise of power. It is also vital for protecting individual rights and ensuring that the government is accountable to the people.

A market-based economy is characterized by private ownership of property and free exchange of goods and services. This principle fosters economic growth and prosperity, and provides individuals with the opportunity to pursue their own economic interests. It also provides a check on government power by limiting the state’s ability to interfere with the economy.

Representative government is based on the idea that citizens have the right to elect their leaders and hold them accountable for their actions. This principle is essential for ensuring that government is responsive to the needs and desires of the people, and that power is distributed fairly.

4) What do you understand by a natural monopoly? Why are public utilities usually natural monopolies?

Ans: A natural monopoly is a market situation where the most efficient producer can supply the entire market at a lower cost than any potential competitor. In other words, it is a market in which the economies of scale are so significant that it is economically efficient for one firm to produce and supply the entire market. As a result, the market cannot support more than one firm.

Public utilities, such as water, electricity, and gas, are often natural monopolies because they require significant infrastructure and fixed costs to provide their services. For example, it would be prohibitively expensive for multiple companies to lay separate sets of pipes to provide water or gas to every household in a given area. Instead, it is more efficient to have a single utility company that can provide these services at a lower cost due to economies of scale.

In addition, public utilities are often regulated by government bodies to prevent them from abusing their market power. This regulation can help ensure that prices are fair and that the quality of service is maintained, which is important because public utilities are essential services that people rely on for their daily needs.

5) Explain the Learning-by-Doing model of Kenneth Arrow.

Ans: Kenneth Arrow’s Learning-by-Doing model is a theory that suggests that firms can learn and improve their productivity by producing more output. In other words, firms can become more efficient and productive over time as they gain more experience and knowledge through the process of producing goods and services.

According to this model, there are two types of knowledge that firms can acquire: explicit and tacit. Explicit knowledge can be easily codified and transmitted, such as through books, manuals, and training programs. In contrast, tacit knowledge is more difficult to codify and is acquired through experience and learning by doing.

As firms produce more output, they develop specialized skills and knowledge that improve their productivity and efficiency. This can lead to a reduction in costs, better quality control, and more efficient production processes. As a result, firms that have been in the market for a longer time may have a competitive advantage over new entrants, as they have already accumulated a significant amount of tacit knowledge.

The Learning-by-Doing model has important implications for economic growth and technological progress. As firms gain more experience and knowledge, they can develop new and better ways of producing goods and services, leading to improvements in productivity and economic growth. In addition, the model suggests that government policies that promote investment and innovation can help firms acquire new knowledge and improve their productivity, leading to economic development.

C. Short Answer Questions (word limit 100 words)

6) Differentiate between:

(a) Exogenous Growth and endogenous growth.

Ans: Exogenous growth and endogenous growth are two different approaches to explaining how an economy grows.

Exogenous growth refers to a theory that explains economic growth through external factors, such as technological advancements, investment in physical capital, or population growth. Exogenous growth suggests that economic growth is driven by factors outside of the economic system, and that policy interventions can be used to promote growth.

Endogenous growth, on the other hand, suggests that economic growth is driven by internal factors, such as human capital, research and development, and innovation. Endogenous growth theory suggests that economies can grow sustainably over the long term by investing in education and research and development, and that these investments can be self-sustaining.

(b) Capital-augmenting technical change and capital-deepening technical chane.

Ans: Capital-augmenting technical change and capital-deepening technical change are two different types of technological changes that affect the production process and economic growth.

Capital-augmenting technical change refers to a type of technological change that increases the productivity of capital goods. This means that the same amount of capital can produce more output than before. Examples of capital-augmenting technical change include improvements in machinery, tools, or equipment.

Capital-deepening technical change refers to a type of technological change that increases the amount of capital per worker in the production process. This means that each worker has access to more capital, which can lead to higher levels of productivity and economic growth. Examples of capital-deepening technical change include investments in new capital goods, such as machinery or equipment, or improvements in the quality of existing capital goods.

In general, both types of technological changes can lead to increases in economic growth and productivity. However, the impact of each type of technological change may vary depending on the specific economic context and the level of development of the economy.

(c) Market Failure and Government Failure.

Ans: Market failure and government failure are two different concepts related to the inability of markets or governments to achieve desirable outcomes.

Market failure occurs when the market fails to allocate resources efficiently or achieve socially optimal outcomes. There are several reasons why market failure can occur, including externalities, public goods, imperfect competition, information asymmetry, and income inequality. In these cases, the market may lead to outcomes that are not efficient or equitable, and may require government intervention to correct.

Government failure occurs when government policies or interventions fail to achieve their intended goals, or when the costs of government intervention exceed their benefits. Government failure can occur due to a variety of reasons, including bureaucratic inefficiencies, regulatory capture, rent-seeking, corruption, and unintended consequences of policies. In these cases, government intervention may lead to outcomes that are worse than the market outcomes, and may require reforms or changes to improve the effectiveness of government policies.

Both market failure and government failure can lead to suboptimal outcomes and the need for policy interventions. The challenge is to identify the specific causes of failure and design policies that can correct or mitigate the problem, while minimizing the costs and unintended consequences of policy interventions.

7) Write short notes on the following.

(a) Lorenz Curve.

Ans: The Lorenz curve is a graphical representation of the degree of income inequality in a society. It plots the cumulative share of total income received by each percentile of the population against the cumulative percentage of the population, starting from the poorest to the richest. The Lorenz curve shows how far the actual distribution of income deviates from an equal distribution. If the Lorenz curve lies below the line of perfect equality, it indicates that income is concentrated in the hands of a few, and the society is more unequal. On the other hand, if the Lorenz curve is closer to the line of perfect equality, it suggests a more equal distribution of income. The Lorenz curve is commonly used to measure income inequality and is a useful tool for policymakers to assess the distribution of income and design policies to reduce inequality.

(b) Growth Accounting.

Ans: Growth accounting is an analytical tool used by economists to understand the sources of economic growth in a country or region. It involves decomposing the change in output, usually measured as gross domestic product (GDP), into contributions from different factors of production, such as labor, capital, and technology.

The basic idea behind growth accounting is that changes in GDP can be explained by changes in the inputs used to produce it. In particular, changes in output can be attributed to changes in the quantity and quality of labor, changes in the quantity and quality of capital, and changes in the level of technology.

Growth accounting can be used to identify the sources of economic growth and to compare the performance of different countries or regions over time. For example, if one country experiences faster economic growth than another, growth accounting can be used to determine whether the difference is due to differences in labor productivity, capital accumulation, or technological progress.

Growth accounting can also be used to inform policy decisions. For example, if growth accounting suggests that a particular country is experiencing slow economic growth due to a lack of investment in physical or human capital, policymakers may consider measures to encourage investment, such as tax incentives or education and training programs.

(c) Convergence.

Ans: Convergence is an economic concept that refers to the tendency of economies to grow and converge to a common steady-state level of output per capita. In other words, convergence suggests that poorer countries or regions will tend to catch up to richer ones in terms of economic growth and income per capita over time.

The concept of convergence is based on the idea that poorer economies have more room for growth than richer economies, which are closer to their technological and productivity limits. As poorer economies invest in physical and human capital, adopt new technologies, and become more productive, they can experience faster economic growth rates than richer economies. However, as they converge towards higher levels of output per capita, their growth rates will slow down and eventually stabilize.

Empirical evidence suggests that convergence does occur, although the process can be slow and vary across countries and regions. Convergence can be affected by factors such as institutions, policies, trade openness, and human capital. Countries with better institutions, more favorable policies, and higher levels of human capital tend to converge more quickly than those with weaker institutions, less favorable policies, and lower levels of human capital.

Convergence has important implications for global economic development and inequality. If convergence occurs, it suggests that the income gap between rich and poor countries will gradually narrow over time. However, if convergence is slow or does not occur, it can lead to persistent income inequality and differences in living standards between countries.

How to Download BECC-112 Solved Assignment?

You can download it from the www.edukar.in, they have a big database for all the IGNOU solved assignments.

Is the BECC-112 Solved Assignment Free?

Yes this is absolutely free to download the solved assignment from www.edukar.in

What is the last submission date for BECC-112 Solved Assignment?

For June Examination: 31st April, For December Examination: 30th October

")

")

")

")

")

")

")